The GEX suite surfaces three specific price levels for every analyzed ticker: the Call Wall, the Put Wall, and the Gamma Flip. Each one represents a different feature of dealer option positioning, and each one has different implications for short-term price action. This page explains what each level is, how dealer hedging behaves around it, and how to use them together.

Before you start

Required:

- Basic understanding of what GEX measures. See Understanding GEX if you haven't read it yet.

Time to complete: 10 minutes

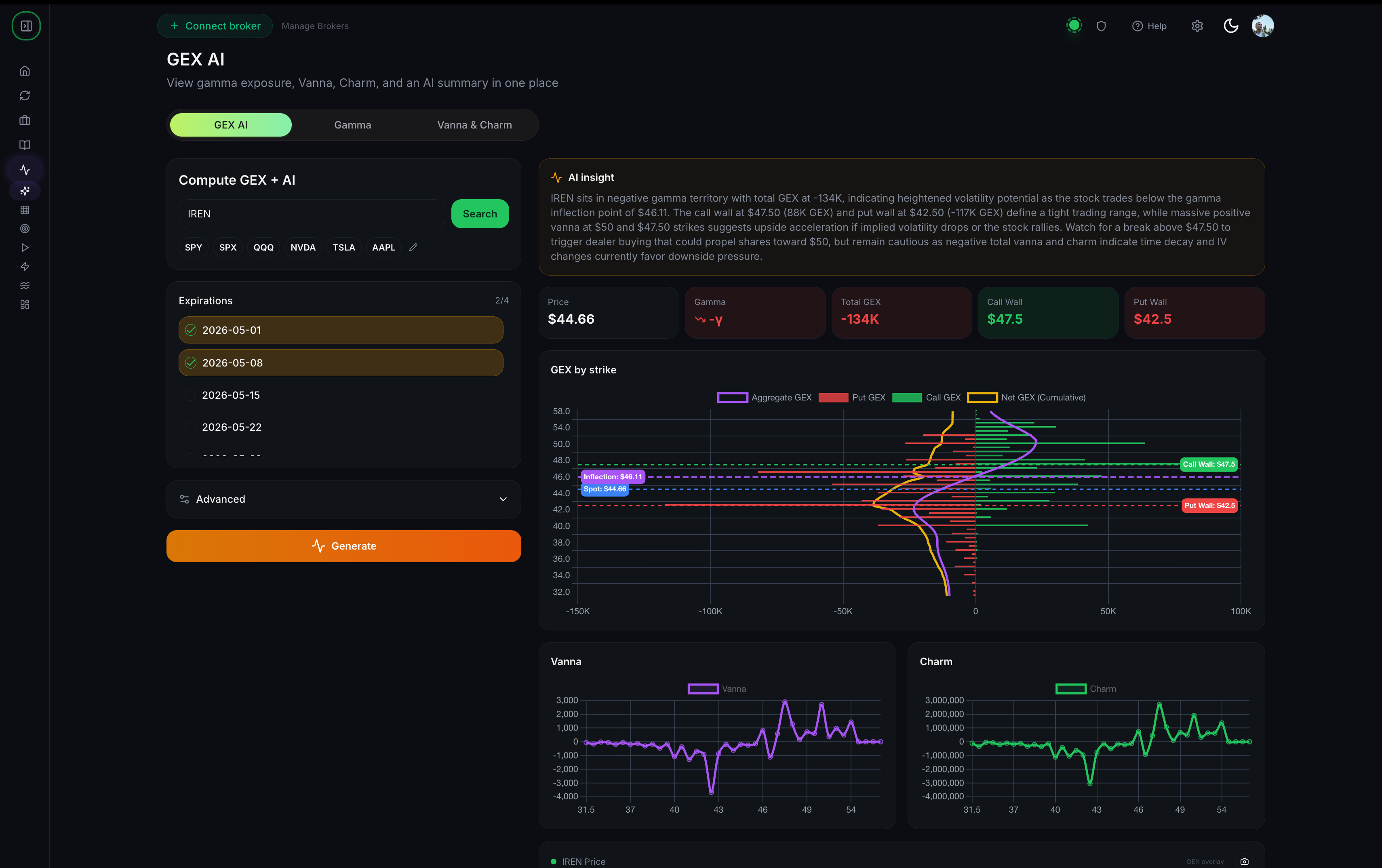

The Call Wall

Definition. The Call Wall is the strike with the largest concentration of net positive gamma exposure from open call contracts. It's where dealer hedging, as a function of price movement, is strongest on the call side.

What dealers do there. At the Call Wall, dealers have sold a lot of calls at or near that strike. They're hedged against those calls by holding some amount of the underlying. As the stock price approaches the Call Wall, dealer gamma increases rapidly — each additional $1 of stock movement forces bigger hedging trades. Because dealers are typically short gamma on calls they've sold, their hedging at the Call Wall pushes back against upward moves.

Practical result: prices often stall or reverse when approaching the Call Wall from below. This isn't a guarantee — news, earnings, macro events can break any technical level — but it's a statistical tendency observable across many tickers and sessions.

When the Call Wall breaks. If price decisively breaks above the Call Wall, two things change:

- The gamma-hedging dynamic flips. Dealers now need to buy more stock to stay hedged as price rises further.

- The new Call Wall (at a higher strike) becomes the next resistance level.

Breakouts above the Call Wall often lead to accelerated upside moves — a "gamma squeeze" — because dealer buying adds to the move rather than resisting it.

The Put Wall

Definition. The Put Wall is the strike with the largest concentration of net positive gamma exposure from open put contracts. Symmetric to the Call Wall, but on the downside.

What dealers do there. Dealers have sold a lot of puts at or near the Put Wall. As price approaches from above, their gamma position grows. Their hedging at the Put Wall pushes back against downward moves — typically by buying the stock as it falls toward the Put Wall.

Practical result: prices often find support when approaching the Put Wall from above. Often but not always; same caveats as the Call Wall.

When the Put Wall breaks. Decisive breakdown below the Put Wall flips the hedging dynamic. Dealers who were buying to hedge short puts now need to sell as price continues falling — accelerating the decline. This is one of the mechanics behind sharp selloffs that seem to "cascade."

The Gamma Flip

Definition. The Gamma Flip is the price level where net dealer positioning transitions between long-gamma (stabilizing) and short-gamma (destabilizing), aggregated across all strikes.

What changes at the flip.

- Above the Gamma Flip (often, depends on positioning): dealers are net long gamma. Their hedging is contrarian — they sell into rallies and buy into dips, which dampens moves. Intraday trading feels mean-reverting.

- Below the Gamma Flip: dealers are net short gamma. Their hedging is pro-cyclical — they buy into rallies and sell into dips, which amplifies moves. Intraday trading feels trending or trending-with-big-swings.

The flip level itself isn't usually a support/resistance line the way walls are. It's more like a regime boundary — you're in a different trading environment on each side of it.

Why it matters. Options traders use GEX regime as a framework for deciding whether to bet on mean reversion or on trend continuation. In long-gamma regimes, fades and range trades work. In short-gamma regimes, breakouts and trend-following work. Getting this wrong — trying to fade a breakout in a short-gamma regime — is how systematic mean-reversion strategies get blown up.

Reading the three levels together

The Call Wall, Put Wall, and Gamma Flip give you a three-point map of the session's structure:

If Price is between the Put Wall and the Gamma Flip: you're in a short-gamma regime with nearby downside support. Breakdowns below the Put Wall could accelerate; holding the Put Wall makes bullish reversals meaningful.

If Price is between the Gamma Flip and the Call Wall: you're in a long-gamma regime with nearby upside resistance. Mean-reversion setups have structural tailwinds; breakouts above the Call Wall could trigger a squeeze.

If Price is above the Call Wall: the market has broken the most-hedged upside level. Dealer hedging is now pro-cyclical on the upside.

If Price is below the Put Wall: downside hedging is pro-cyclical. Often accompanies volatile, trending-down sessions.

The levels update intraday as open interest changes — new option trades shift dealer positioning. The Gamma Flip especially can move meaningfully in a session with heavy option flow.

When to ignore these levels

GEX-derived levels are statistical tendencies, not guarantees. They work best when:

- The ticker has heavy, liquid options activity (SPY, SPX, QQQ, NVDA, TSLA, AAPL, and similar)

- The session is in a normal news/flow environment

- No major macro event is pending (FOMC, CPI, earnings)

They work worst when:

- Major news drives the tape and option hedging is dominated by event risk rather than open interest

- Implied volatility is expanding rapidly (levels become less reliable as vol repositions)

- Open interest is unusually thin (small market makers have little gamma to hedge)

Use walls and flip as context, not as trading signals on their own. A bullish setup at the Put Wall is stronger than the same setup mid-range. A bearish setup at the Call Wall has more room for reversal. The level provides asymmetry; your own setup provides entry.

Common misconceptions

"The Call Wall is always resistance."

It's resistance under normal conditions, but it becomes an accelerant if broken. One-sided framing misses the squeeze dynamic.

"The Gamma Flip is a single number that stays put."

It moves intraday with option flow. Major flips (index options expiring, big put selling) can shift it significantly over a session.

"I should short at the Call Wall and buy at the Put Wall."

Levels are context, not signals. Plenty of sessions break the Call Wall or Put Wall cleanly — if you blindly fade every touch, you'll be run over by the breakouts. Combine levels with your own signal (volume, price action, news).

"Long-gamma regime means bullish."

Long-gamma means stable — rangebound or mean-reverting, not directional. Both bulls and bears expect less trending action in long-gamma environments.

Related

- Understanding GEX and what it tells you

- How to read the GEX Heatmap

- How to track gamma flip events and set alerts

Risk disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and is not investment advice.