Vanna and Charm are second-order Greeks that complement GEX. Where GEX measures dealer hedging flows driven by price moves, Vanna measures dealer hedging driven by implied-volatility changes, and Charm measures dealer hedging driven by the passage of time. All three matter, but they matter in different market conditions — GEX on trending days, Vanna during volatility events, Charm around expiration.

Before you start

Required:

- QuantWheel GEX or QuantWheel PRO subscription.

- Familiarity with GEX. See Understanding GEX and How to use GEX AI for a ticker first. Vanna and Charm build on GEX concepts.

Time to complete: 8 minutes

Where to find them

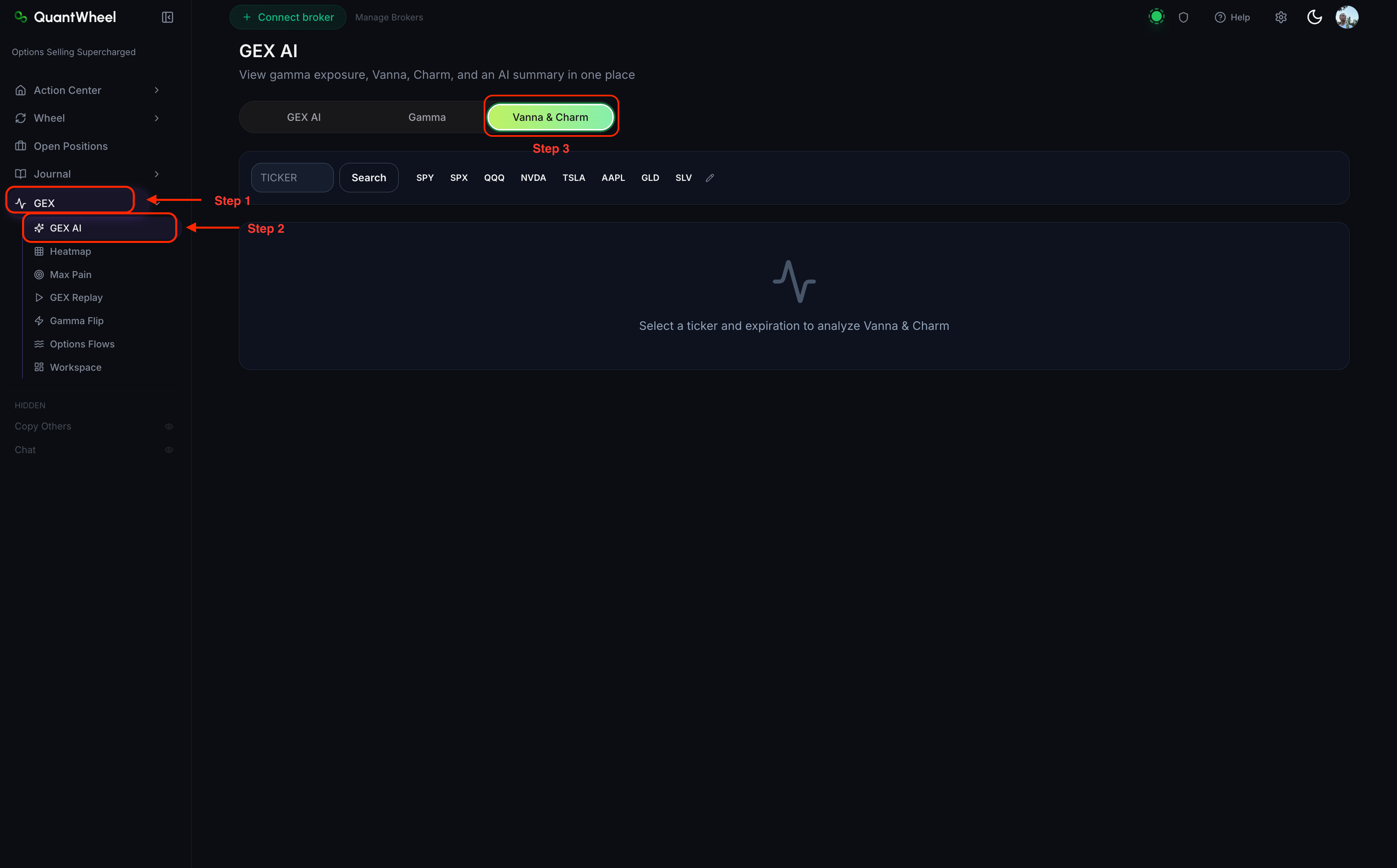

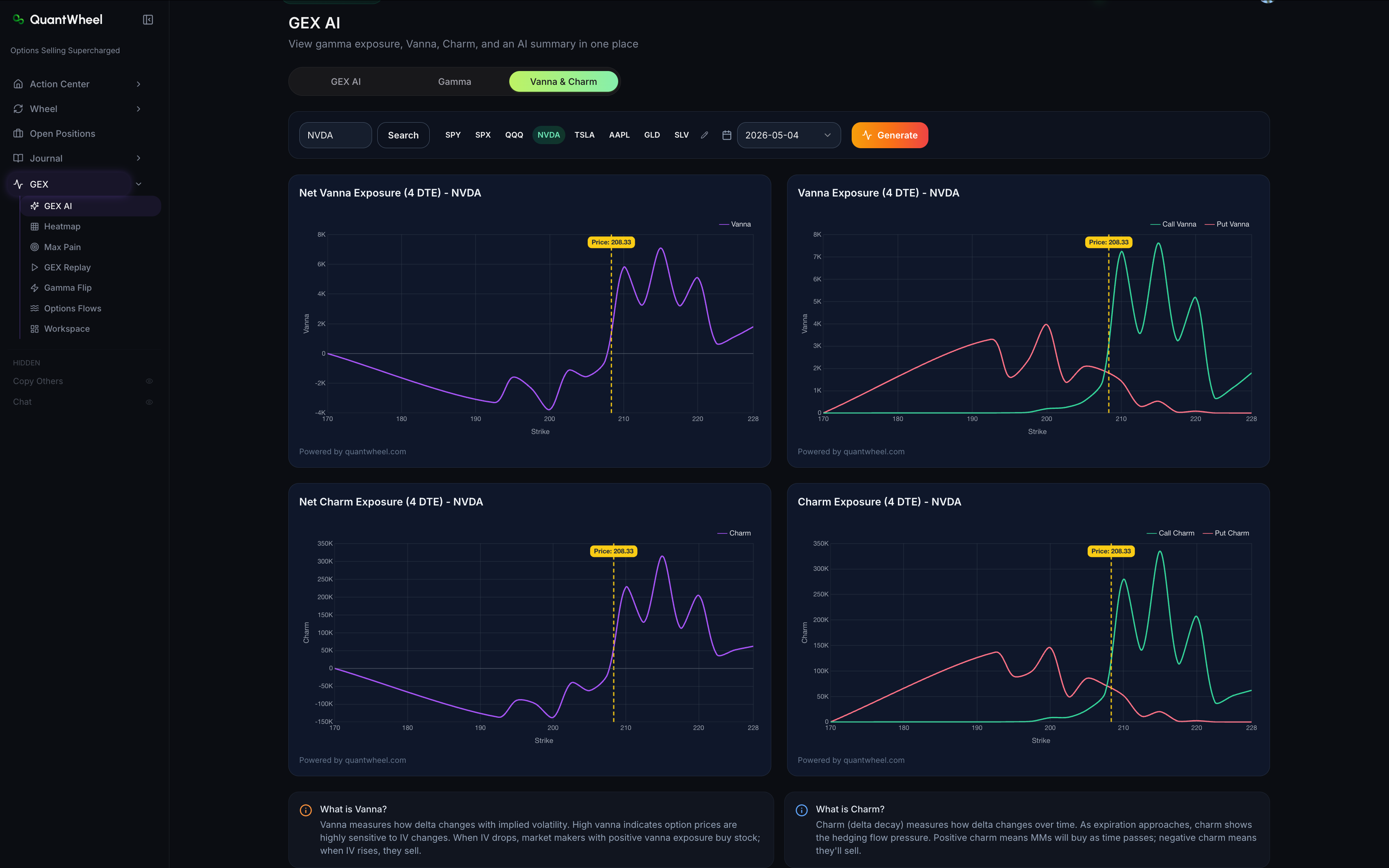

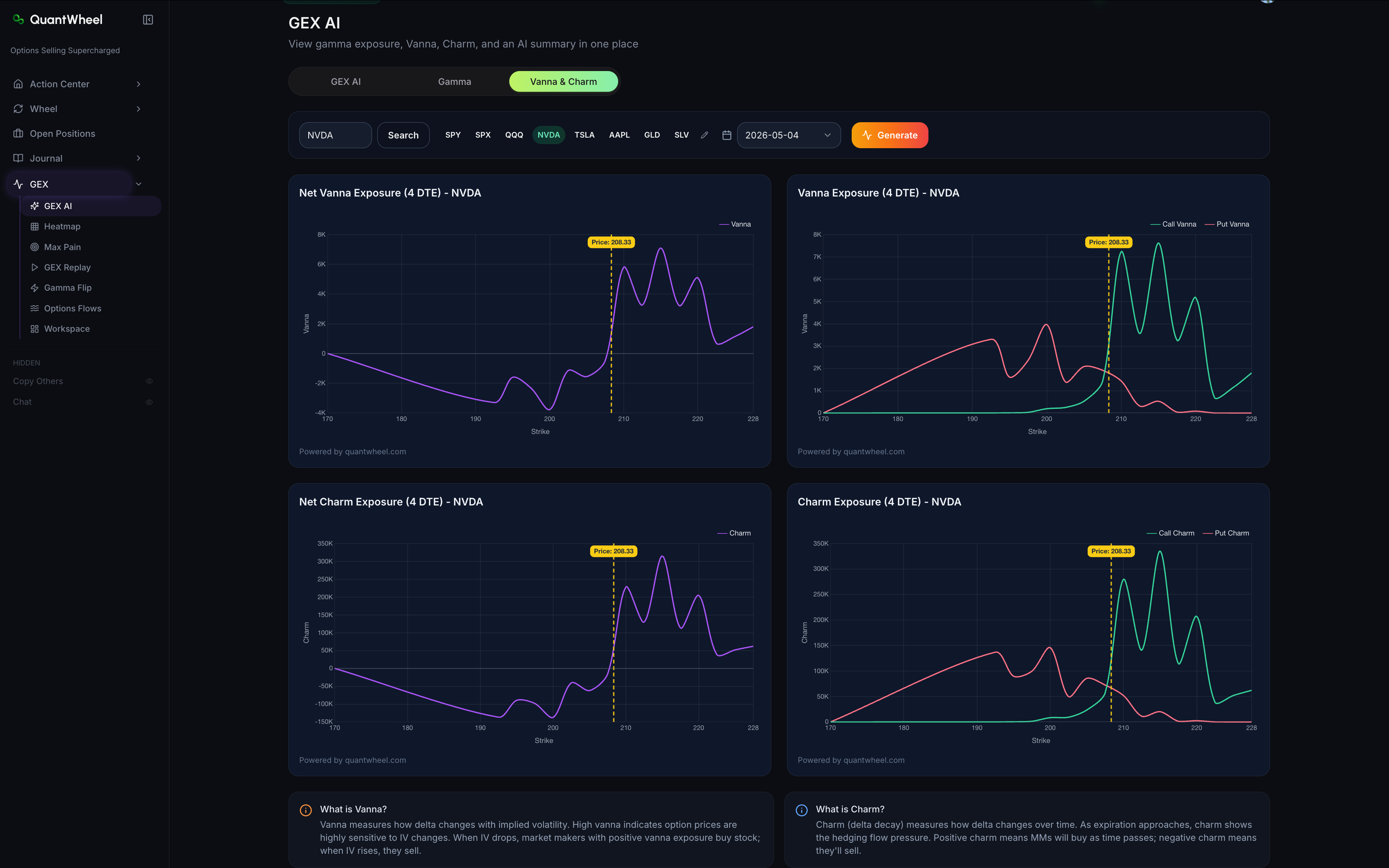

Vanna and Charm live in the GEX AI tab on the left hand side. After clicking to the "vanna & charm" button, write down a ticker you're interested in and choose expiration date. Then click "Search". Next screenshot shows the results of a search.

The section includes four charts plus in-UI explainer boxes labeled "What is Vanna?" and "What is Charm?" — small educational callouts for quick reference.

What Vanna is

Vanna is the rate at which an option's delta changes when implied volatility changes. In dealer-positioning terms:

- If a dealer is short a call option and implied volatility rises, their effective delta on that position changes (typically becomes more negative)

- To stay hedged, the dealer must sell more of the underlying

- Across a large book of options, this volatility-driven hedging can move prices meaningfully

When Vanna matters

- During IV expansion (volatility spikes): dealer Vanna positioning becomes a significant flow. Stocks can move more than "news warrants" because of hedging cascades.

- During IV crush (post-earnings, post-FOMC): the reverse flow — dealer hedging as IV collapses often stabilizes or even reverses moves.

- In persistent low-vol regimes: Vanna effects are quiet and GEX dominates.

The two Vanna charts

QuantWheel typically displays two Vanna views:

- Net Vanna Exposure — total dealer Vanna across strikes and expirations, as a single line over time or a single summary number

- Vanna Exposure (Call/Put) — split into call-side Vanna and put-side Vanna, so you can see which side of the book is driving the exposure

What Charm is

Charm is the rate at which an option's delta changes as time passes (holding everything else constant). In dealer-positioning terms:

- Options decay toward expiration. Their delta drifts — out-of-the-money options drift toward 0 delta, in-the-money options drift toward 1 (or -1) delta.

- Dealers need to adjust their stock hedge every day just to account for this time-driven delta drift.

- The cumulative dealer flow from Charm is typically called "Charm flows" and is most significant near expiration.

When Charm matters

- The last week before a major expiration (OPEX Friday): Charm flows concentrate as delta drift accelerates

- Overnight and into Monday mornings: weekend-and-weekday Charm flows are consistent even without news

- The last hour of expiration day: Charm can dominate all other flows

The two Charm charts

- Net Charm Exposure — total dealer Charm flow, typically across the full book

- Charm Exposure (Call/Put) — split by call-side vs. put-side, useful for spotting asymmetric positioning

How to use Vanna and Charm

For volatility-event trading

Before and during FOMC, CPI, earnings, and similar IV-sensitive events, check Vanna. If the ticker carries large positive Vanna at current strikes, IV spike could trigger significant dealer selling (flow accelerates downside). If negative Vanna, the spike could trigger dealer buying instead.

This is one of the harder GEX concepts to internalize but one of the most useful for event traders.

For expiration-week trading

In the week before OPEX, Charm becomes a meaningful flow. Large positive net Charm in the book suggests dealers need to sell stock daily just to stay hedged; large negative suggests the reverse. This can produce systematic morning flows in the days leading up to expiration.

Pair with Max Pain for the complete expiration-week picture. See How to find max pain strikes.

For overnight gap dynamics

Pre-market gaps on major indices often involve Vanna flow from overnight IV changes (e.g., Asian or European session moves). Tickers with big Vanna exposure can see amplified gap continuations or reversals at the US open.

Not for day-trading most tickers

Most non-event trading days, Vanna and Charm flows are small relative to GEX. Checking them daily for every ticker is overkill. Check them when conditions call for it: around scheduled events, during IV regime changes, and in expiration week.

Common misconceptions

"Vanna and Charm are just smaller versions of GEX."

They're different flow types. GEX responds to price moves. Vanna responds to IV moves. Charm responds to time passing. All three run on different schedules and matter in different conditions.

"These are too advanced to use."

The ideas are conceptually dense, but the practical application is simple: "Check Vanna before IV events. Check Charm in expiration week. Ignore otherwise." Most trading days, GEX alone is the primary GEX-suite signal.

"The Vanna number tells me which way to trade."

Like GEX, Vanna describes dealer positioning, not direction. High positive Vanna tells you dealers will sell more if IV rises — it doesn't tell you whether IV will rise. Combine with your own view on the event.

"Charm always supports mean reversion into expiration."

Sometimes yes, sometimes no. Direction depends on which side of the book Charm flow concentrates on. Read the call-side vs. put-side Charm split, not just net Charm.

Related

Risk disclaimer: Options trading involves substantial risk of loss and is not suitable for all investors. Past performance does not guarantee future results. This content is for educational purposes only and is not investment advice.